Articles

Bitcoin is testing a key trendline. Reversal or breakout ahead?

April 14, 2025 16:14 Forexlive Latest News Market News

The pause in reciprocal tariffs last Wednesday boosted Bitcoin and risk assets in general as growth fears eased and the market started to look forward to more de-escalation ahead.

We also got some exemptions last Friday on tech which helped risk assets but Trump eventually poured cold water on positive expectations as he said that they will be short-lived and they are planning for new tariffs.

On the daily chart above, we can see that Bitcoin is now trading right at the key trendline. This is where we can expect the sellers to step in with a defined risk above the trendline to position for a drop into the 70,000 level. The buyers, on the other hand, will want to see the price breaking higher to start targeting the 90,625 level next.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

The bond market stays on edge in the new week

April 14, 2025 15:39 Forexlive Latest News Market News

This is still one of the more important spots to watch with regards to the whole trade war and tariffs saga at the moment. Yields blowing up in the past week was a key reason in prompting a U-turn from Trump on his reciprocal tariffs policy. And despite scaling back on tariffs on key electronics over the weekend, the bond market remains in a tricky spot to start the week.

In the equities space, there is some hopeful optimism. But for Treasuries, there is still some apprehension. 30-year yields at 4.87% are still on the high side and holding more than 50 bps above the lows from early last week. Even 10-year yields are at 4.46% currently, and likewise is some 58 bps above the lows from last week.

If you want to switch it around, 30-year yields are down just 15 bps from the high last week of 5.02%. Meanwhile, 10-year yields only down by 13 bps from the high last week of 4.59%.

Taking all of that in, it indicates that the bond market remains very much on edge in the new week. Traders will be looking to what Trump will do next but if anything, it will take some time or some bigger gesture to calm the nerves here.

This article was written by Justin Low at www.forexlive.com.

Risk of a significant global slowdown has increased considerably – German economy ministry

April 14, 2025 15:30 Forexlive Latest News Market News

- Effects of US tariffs are not yet reflected in current economic indicators

- The risk of a significant global slowdown has increased considerably

- That will also have an impact on the German economy

- Uncertainty about development of German exports is exceptionally high due to tariffs policy

Just when you think the German economy might be turning a corner, then US tariffs are now going to kick in. With a surging euro, it only adds to concerns about the situation for the industrial sector and exports. Will the ECB be quietly thinking about a 50 bps rate cut?

This article was written by Justin Low at www.forexlive.com.

Key events for the week 14-18 April

April 14, 2025 15:14 Forexlive Latest News Market News

UPCOMING

EVENTS:

- Monday: New Zealand Services PMI, NY Fed Consumer Inflation

Expectations. - Tuesday: RBA Meeting Minutes, UK Employment Report, German

ZEW, Canada CPI. - Wednesday: Japan Tankan, China Industrial Production and

Retail Sales, UK CPI, US Retail Sales, US Industrial Production and

Capacity Utilisation, BoC Policy Announcement, US NAHB Housing Market

Index, Fed Chair Powell. - Thursday: New Zealand Q1 CPI, Australia Employment

report, ECB Policy Announcement, US Housing Starts and Building Permits,

US Jobless Claims. - Friday: Japan CPI (Good Friday Holiday)

Tuesday

The UK

Unemployment Rate is expected to remain unchanged at 4.4%. The Average Earnings

are expected at 5.7% vs. 5.8% prior, while the Ex-Bonus Earnings are seen at 6.0%

vs. 5.9% prior. The data is unlikely to influence market expectations as the

focus remains on the tariff negotiations and the US-China developments. The

market is currently pricing 76 bps of easing by year-end with an 85%

probability of a 25 bps cut at the upcoming meeting.

The Canadian CPI

Y/Y is expected at 2.6% vs. 2.6% prior, while the M/M reading is seen at 0.6%

vs. 1.1% prior. The Trimmed-Mean CPI Y/Y is expected at 3.0% vs. 2.9% prior,

while the Median CPI Y/Y is seen at 3.0% vs. 2.9% prior.

Inflation has been

moving higher recently after the aggressive BoC easing and the tariffs are

expected to keep inflation higher while weighing on growth. The market sees 36

bps of easing by year-end with a 61% probability that the central bank will

hold rates unchanged this week.

Wednesday

The UK CPI Y/Y is

expected at 2.7% vs. 2.8% prior, while the M/M reading is seen at 0.4% vs. 0.4%

prior. The Core CPI Y/Y is expected at 3.5% vs. 3.5% prior, while Services CPI

Y/Y is seen at 4.9% vs. 5.0% prior.

Again, the data this

month is unlikely to influence market’s expectations that much as the focus

remains on tariff negotiations. The market is currently pricing 76 bps of

easing by year-end with an 85% probability of a 25 bps cut at the upcoming

meeting.

The US Retail

Sales M/M is expected at 1.4% vs. 0.2% prior, while the ex-Autos figure is seen

at 0.4% vs. 0.3% prior. The focus will be on the Control Group figure which is

expected at 0.6% vs. 1.0% prior.

Consumer spending

has been stable in the past months which is something you would expect given

the positive real wage growth and resilient labour market. More recently

though, we’ve been seeing some marked easing in consumer sentiment due to the

ongoing trade wars which could weigh on spending going forward.

The BoC is

expected to keep rates unchanged at 2.75%. As a reminder, the BoC cut interest

rates by 25 basis points to 2.75% as expected at the last meeting amid concerns

over weaker growth ahead due to the trade uncertainty and US tariffs. The

central bank emphasized a cautious approach to future decisions, balancing the

upward pressure on inflation against the downward pressure on weaker demand. The

market expects just one last cut by year-end.

Thursday

The New Zealand Q1

CPI Y/Y is expected at 2.3% vs. 2.2% prior, while the Q/Q figures is seen at

0.7 vs. 0.5% prior. The market sees 103 bps of easing by year-end with a 72%

probability of a 50 bps cut at the upcoming meeting. All these market

expectations about interest rates were influenced by the global market rout

following Trump’s aggressive tariffs. That’s where the focus is now. A reversal

or easing in the trade war would diminish the aggressive rate cuts

expectations.

The Australian

Employment report is expected to show 35K jobs added in March vs. -52.8K in February,

and the Unemployment Rate to tick higher to 4.2% vs. 4.1% prior. The US trade

war and the global market selloff pushed the market to expect 107 bps of easing

by year-end with a 40% probability of a 50 bps cut at the upcoming meeting.

The ECB is

expected to cut by 25 bps bringing the deposit rate to 2.25%. The market then

expects at least two more rate cuts by year-end. Interest rates expectations

have been shaped by the ongoing trade war and the recent 90-days pause for

reciprocal tariffs helped to alleviate the aggressive pricing. Again, it’s all

about the trade war now as the data remains old news.

The US Jobless

Claims continue to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims hover

around cycle highs.

This week Initial

Claims are expected at 226K vs. 223K prior, while there’s no consensus for

Continuing Claims at the time of writing although the prior release saw a

decrease to 1850K vs. 1893K prior.

Friday

The Japanese Core

CPI is expected at 3.2% vs. 3.0% prior. Given the global market rout and

aggressive risk off sentiment, traders scaled back their rate hikes

expectations and they now see the BoJ remaining on hold for the rest of the

year. Of course, this is all connected to the trade war so an easing and positive

developments on that front should increase the expectations for a rate hike by

year-end.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

What are the interest rates expectations for G8FX?

April 14, 2025 15:14 Forexlive Latest News Market News

Rate cuts by year-end

- Fed: 81 bps (76% probability of no change at the upcoming meeting)

- ECB: 76 bps (99% probability of rate cut at the upcoming meeting)

- BoE: 75 bps (93% probability of rate cut at the upcoming meeting)

- BoC: 40 bps (58% probability of no change at the upcoming meeting)

- RBA: 118 bps (76% probability of 25 bps rate cut at the upcoming meeting)

- RBNZ: 77 bps (97% probability of rate cut at the upcoming meeting)

- SNB: 25 bps (74% probability of rate cut at the upcoming meeting)

* for the RBA, the rest of the probability is for a 50 bps cut.

Rate hikes by year-end

- BoJ: 10 bps (99% probability of no change at the upcoming meeting)

Since Friday’s update, we can see that traders are getting less aggressive on rate cuts as the stock markets continue to recover and hopes for de-escalation keep on increasing.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

SNB total sight deposits w.e. 11 April CHF 446.9 bn vs CHF 443.7 bn prior

April 14, 2025 15:14 Forexlive Latest News Market News

- Domestic sight deposits CHF 438.4 bn vs CHF 433.4 bn prior

There’s a slight rise in the past week but nothing that stands out all too much. Once markets start to settle down a bit more, this will be an interesting data point to watch in order to gauge the SNB’s intervention appetite. Here’s the trend for the year:

This article was written by Justin Low at www.forexlive.com.

Market Outlook for the Week 14th-18th April

April 14, 2025 14:14 Forexlive Latest News Market News

The week will start off slowly in terms of scheduled economic events, but markets will remain alert to any unexpected announcements from the U.S. administration, particularly regarding potential retaliatory tariffs.

On Tuesday, the U.K. will release the claimant count change, the average earnings index 3m/y, and the unemployment rate. In Canada, attention will turn to inflation data.

Wednesday brings inflation data from the U.K. and retail sales figures m/m from the U.S. In Canada, the focus will be on the Bank of Canada’s monetary policy announcement. Additionally, Fed Chair Powell is scheduled to speak on the economic outlook at the Economic Club of Chicago.

On Thursday, New Zealand will release its inflation data, while Australia will publish employment change and the unemployment rate. The eurozone will also be in focus with the European Central Bank’s monetary policy announcement.

Most major banks will be closed on Friday in observance of Good Friday.

In the U.K., the consensus for the claimant count change is 30.3K vs the prior 44.2K. The average earnings index 3m/y is expected at 5.7%, slightly below the previous 5.8%, while the unemployment rate is projected to remain unchanged at 4.4%.

The labor market is showing signs of cooling, though wage growth has remained relatively strong. In terms of monetary policy, the Bank of England is not finished with rate cuts, particularly as inflation remains elevated and well above the target.

The U.K. CPI y/y is only expected to drop from 2.8% to 2.7% and this is likely because of falling gas prices. However, services inflation is proving to be more stubborn.

In the U.S., the consensus for core retail sales m/m is 0.4% vs. the prior 0.3%, and for retail sales m/m is 1.4% vs. the prior 0.2%.

ING analysts suggest that one of the main reasons for the strong retail sales data may be consumers making major purchases in advance of anticipated tariffs. They highlight a notable 10.6% m/m jump in auto volumes based on Wards data, along with increased credit card spending on appliances and electronics.

Tariff-related uncertainty is expected to persist for the time being, and its impact on future economic data will continue to be closely watched.

Inflation data for Canada will be released on Tuesday ahead of the BoC meeting. The consensus for CPI m/m is 0.7% vs. the prior 1.1%; median CPI y/y is expected to remain unchanged at 2.9%; trimmed CPI y/y is also forecast to hold steady at 2.9%, while common CPI y/y is likely to decline from 2.5% to 2.4%.

Analysts are divided on whether the BoC will deliver a rate cut at this week’s meeting. While recent inflation data has surprised to the upside and uncertainty surrounding tariffs remains elevated, a weakening labor market and economic growth concerns may support the case for another cut. Wells Fargo analysts point to the 32.6K drop in March employment figures and the already deteriorating business sentiment captured by the BoC’s Q1 Business Outlook Survey conducted in February, even before the higher U.S. tariffs went into effect.

In New Zealand, the consensus for the CPI q/q is 0.7% vs. the prior 0.5%, with the annual rate expected at 2.3%. Westpac analysts attribute this to elevated food and fuel costs.

Although inflation is below the RBNZ’s desired midpoint target, it still falls within the 1–3% target range. From a monetary policy perspective, even if inflation surprises to the upside, it is unlikely to shift the Bank’s policy stance in the near term.

In Australia, the consensus for the employment change is 40.2K vs. -52.8K, and the unemployment rate is expected to rise slightly from 4.1% to 4.2%.

After last month’s sharp decline, a solid rebound is anticipated. Analysts from Westpac noted that March is expected to bring a recovery in the participation rate, rising from 66.8% to 67.0%, which would support the employment rebound. Although weather disruptions from Ex-Tropical Cyclone Alfred add some uncertainty, any impact on the data is expected to be limited.

At this week’s meeting, the ECB is widely expected to deliver a 25 bps rate cut to 2.25%. Recently, the Bank had a slightly less dovish tone as the economic situation in Germany and the broader eurozone shows signs of improvement. However, uncertainty surrounding tariffs is expected to add pressure in the near future.

Inflation data in the eurozone has shown continued progress, particularly in core and services inflation, supporting the case for rate cuts. Analysts expect additional 25 bps cuts at the June and September meetings, bringing the deposit rate down to 1.75% by the end of the year.

This article was written by Gina Constantin at www.forexlive.com.

Anzac Day Trading Schedule 2025

April 14, 2025 14:00 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Anzac Day on Friday, 25 April, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Kind regards,

IC Markets Global.

The post Anzac Day Trading Schedule 2025 first appeared on IC Markets | Official Blog.

Dollar selling returns to start European morning trade

April 14, 2025 13:45 Forexlive Latest News Market News

Rain or shine, there’s no love for the dollar at the moment. The greenback continues to fall out of favour amid all the uncertainty still in play with regards to Trump’s tariffs policy. EUR/USD is now moving up by 0.5% back above 1.1400 and continues with the technical breakout to the upside from last week:

As the saying goes, the trend is your friend. And in this case, things remain as they are until there is major change to the trade war landscape.

USD/JPY is also back down by 0.8% to 142.38 while USD/CHF has fallen from around 0.8190 earlier to be down 0.2% to 0.8135 currently.

This article was written by Justin Low at www.forexlive.com.

Switzerland March producer and import prices +0.1% vs +0.3% m/m prior

April 14, 2025 13:41 Forexlive Latest News Market News

Slight delay in the release by the source. Looking at the breakdown, producer prices were seen up 0.1% on the month while import prices were flat in March. From a year-on-year perspective, producer and import prices were seen down 0.1% compared to March 2024.

This article was written by Justin Low at www.forexlive.com.

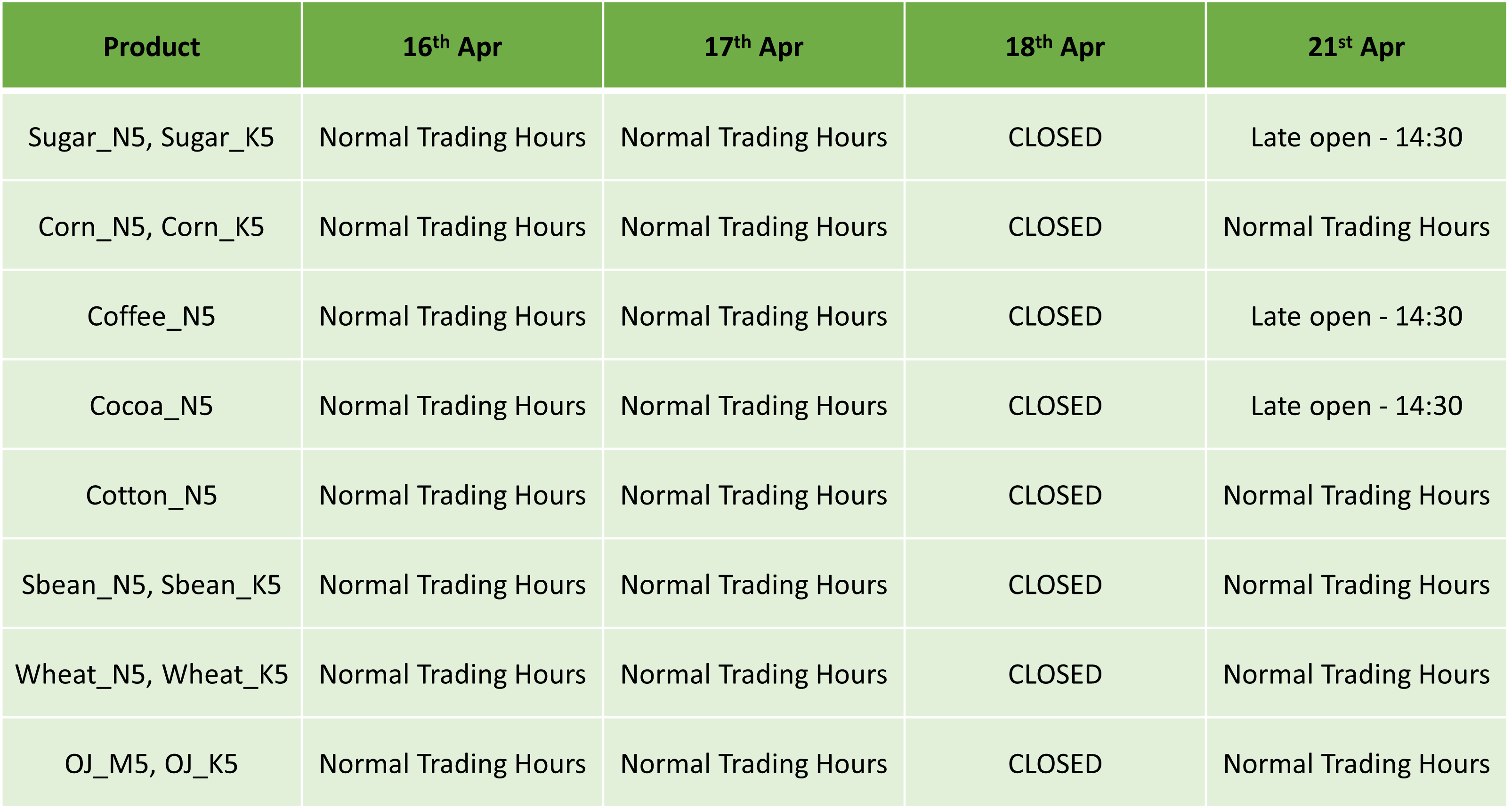

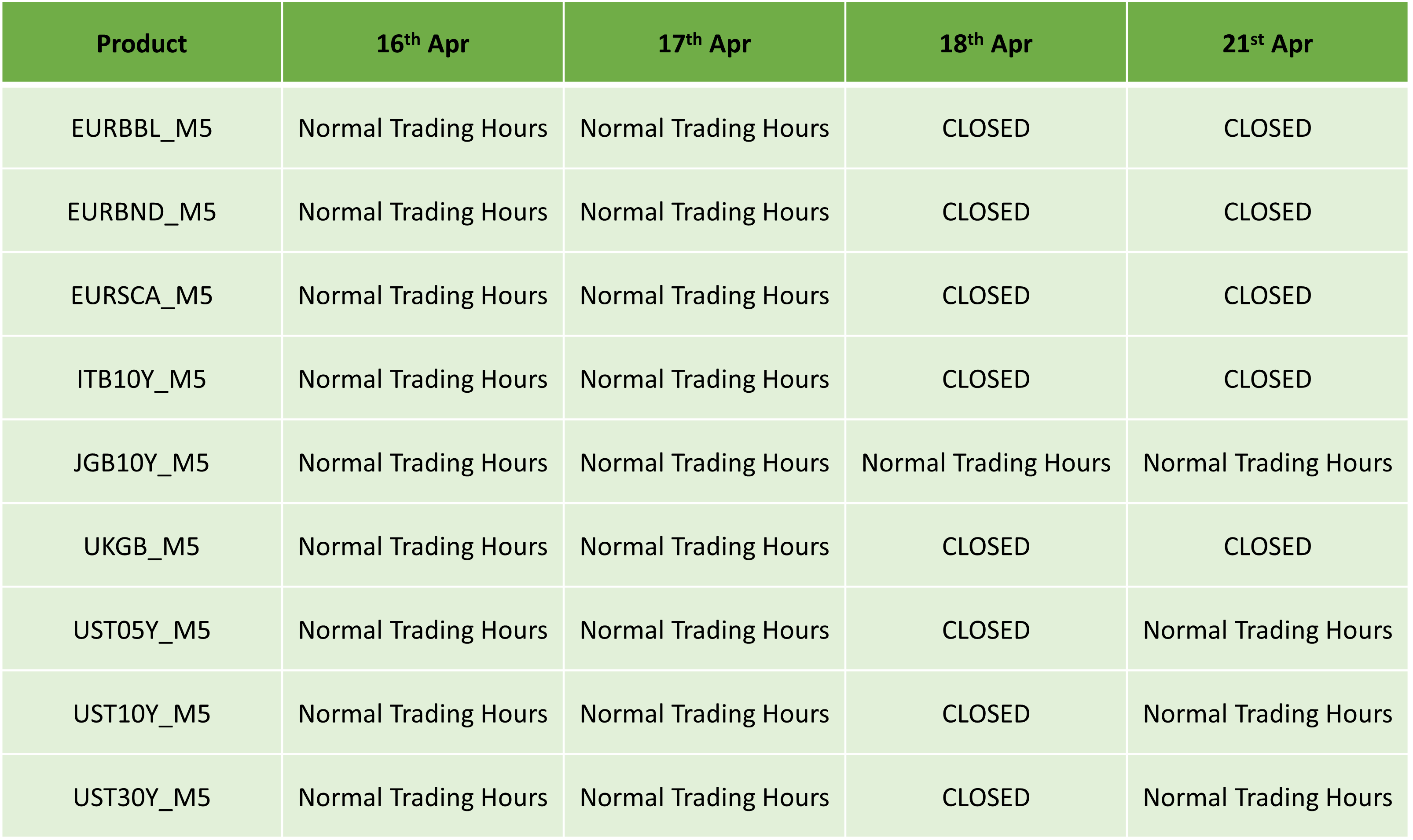

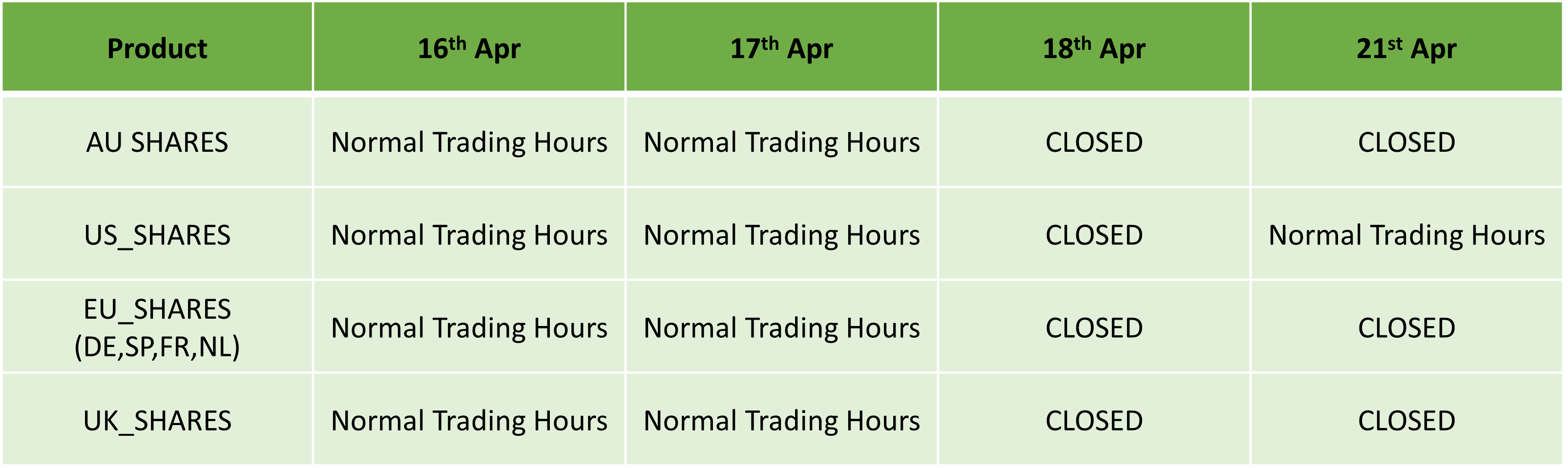

Easter Holidays Trading Schedule 2025

April 14, 2025 13:39 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Easter Holidays starting on Wednesday, 16 April, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Forex / Crypto Pairs:

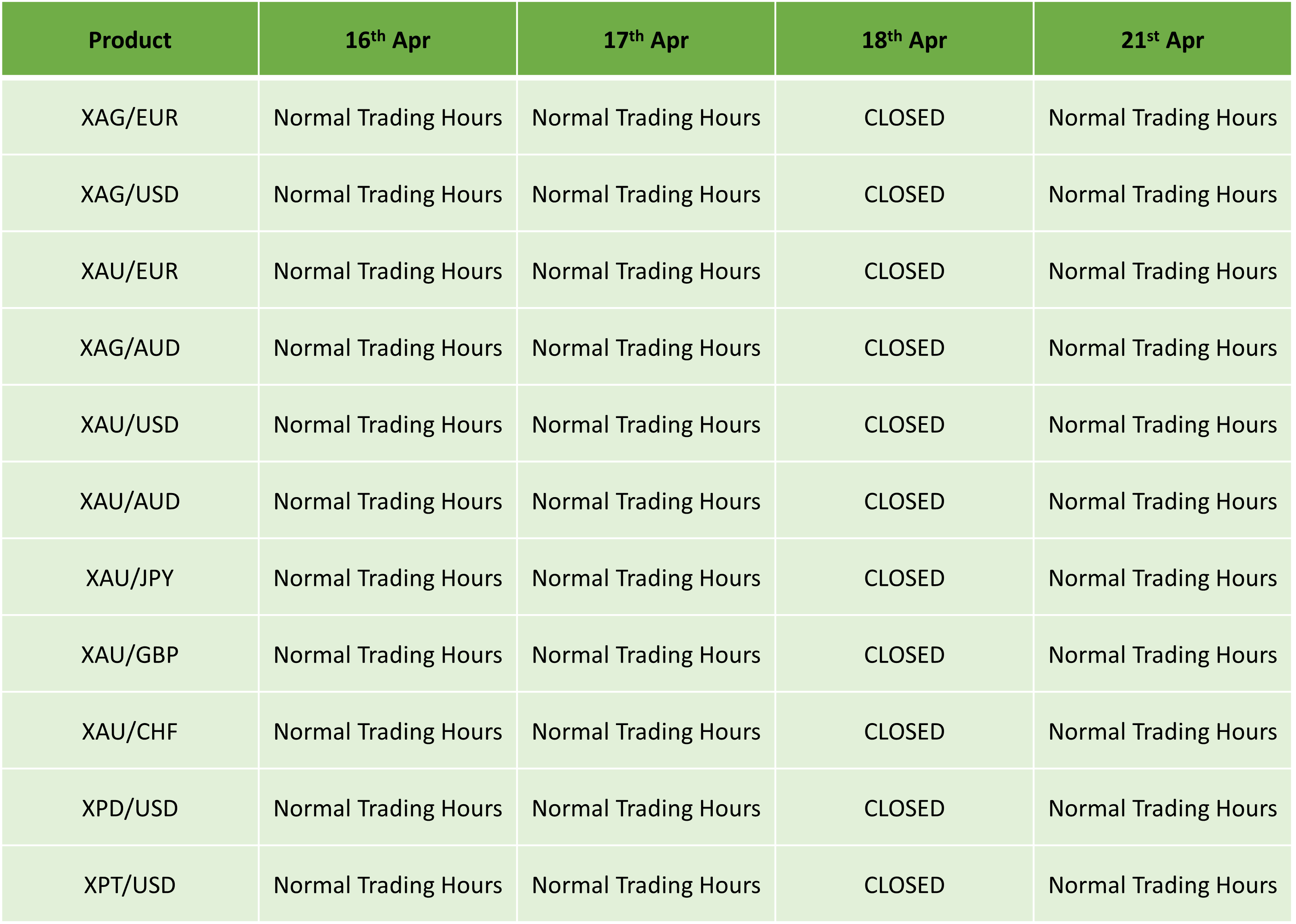

Precious Metals:

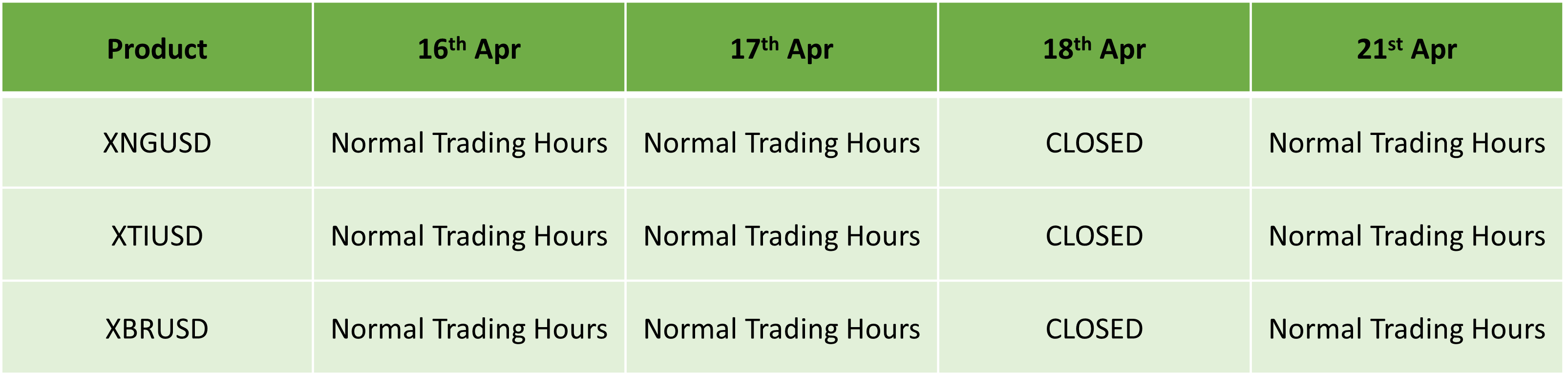

Spot Energies:

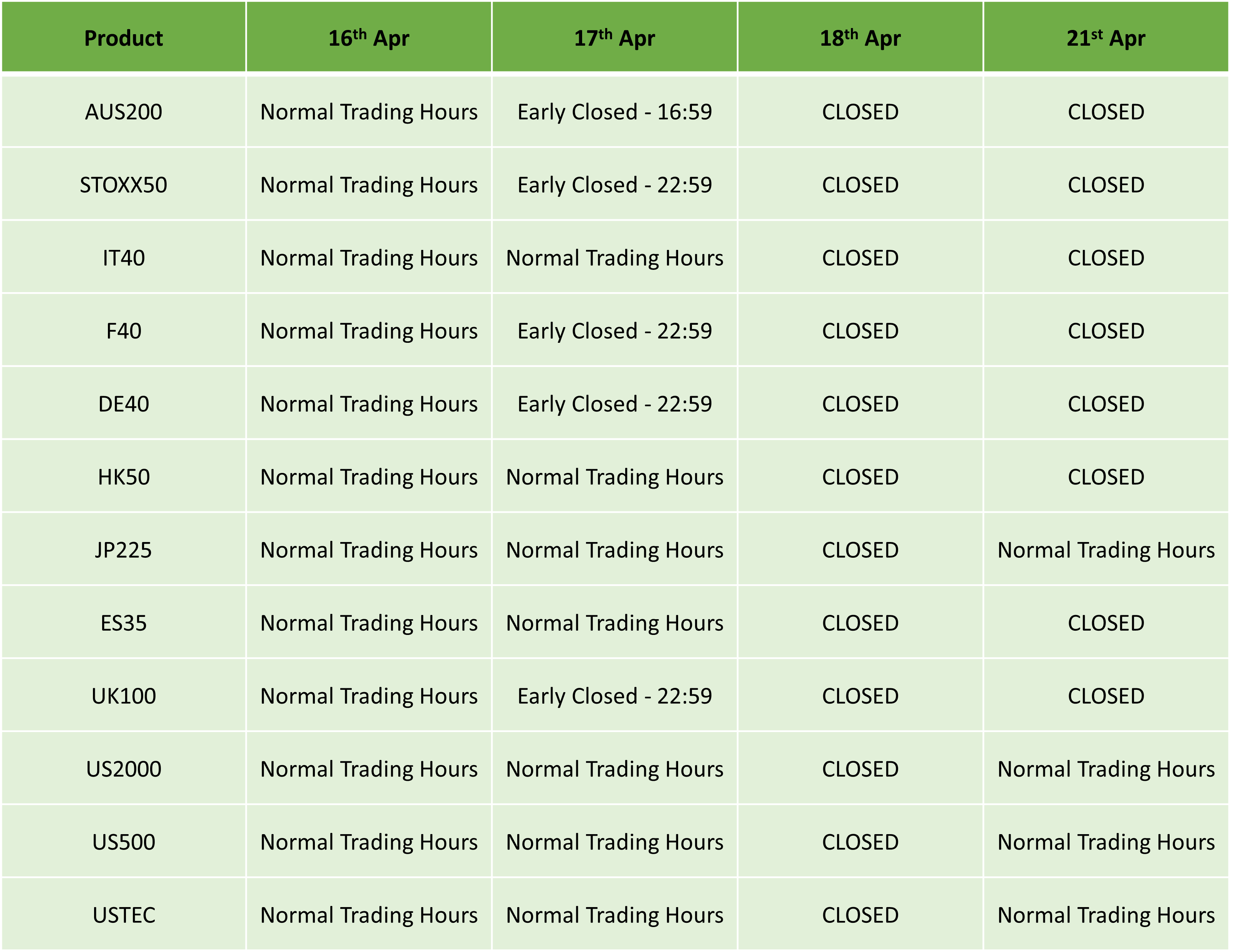

Indices:

Energy Futures:

Soft Commodities Futures:

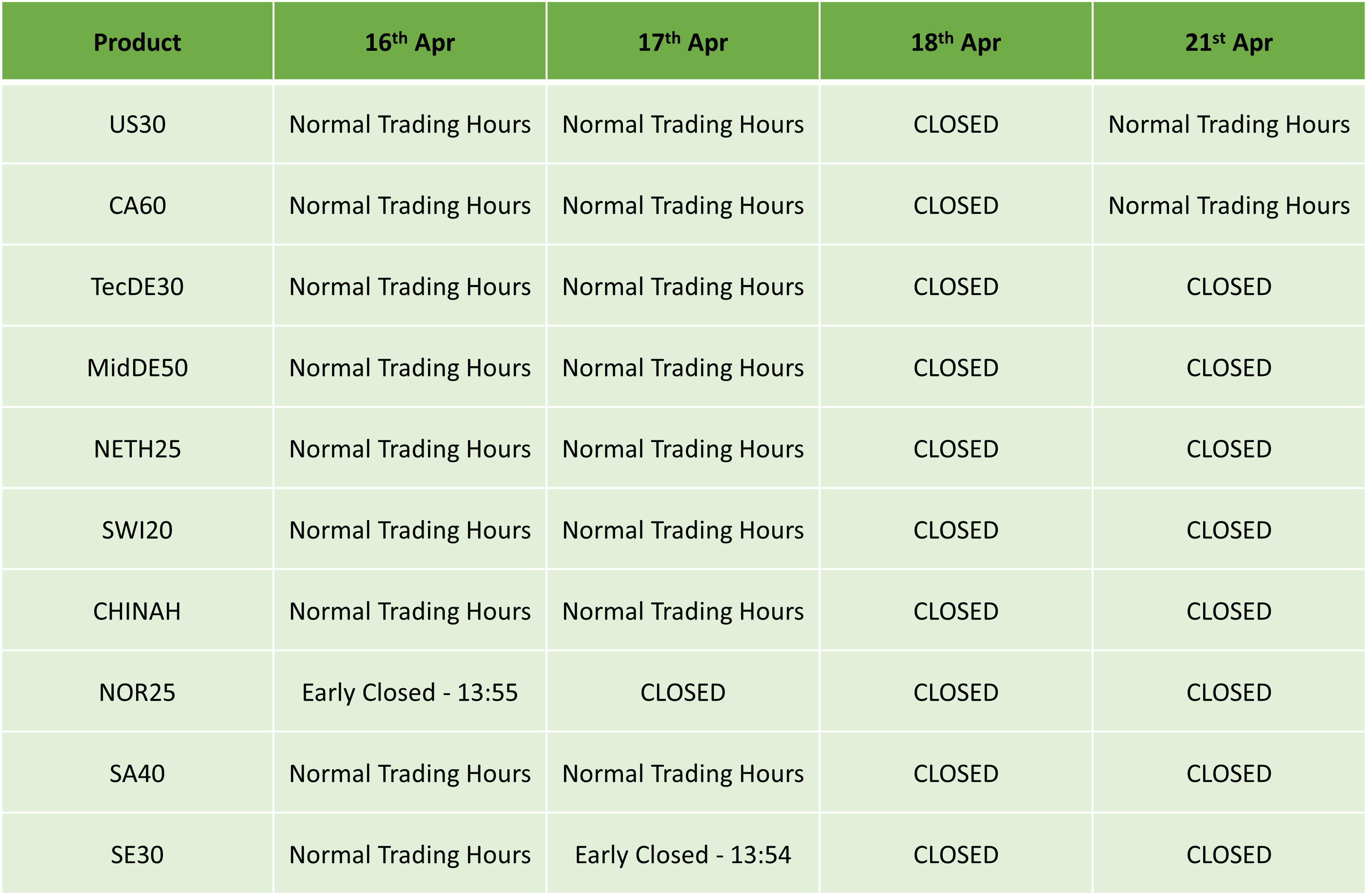

Indices Futures:

Bonds Futures:

Equities:

Kind regards,

IC Markets Global.

The post Easter Holidays Trading Schedule 2025 first appeared on IC Markets | Official Blog.

Trump has directed for tariff talks to begin immediately with South Korea, Japan, India

April 14, 2025 13:14 Forexlive Latest News Market News

These are the US’ closest allies, so you’d expect things to progress a little quicker compared to others. Also, the fact that they’re willing to compromise more I guess. Japan will be speaking with the US later this week as noted here previously.

This article was written by Justin Low at www.forexlive.com.