Articles

Economic calendar in Asia Monday, October 28, 2024 – empty … but check out plunging yen!

407564 October 28, 2024 03:30 Forexlive Latest News Market News

Well, the Japanese election is nail-biter:

Yen has been slammed lower, with USD/JPY above 153.00.

As for the economic calendar, its empty today.

Yne update:

This article was written by Eamonn Sheridan at www.forexlive.com.

Monday morning open levels – indicative forex prices – 28 October 2024 – YEN slammed lower

407563 October 28, 2024 03:14 Forexlive Latest News Market News

Good morning, afternoon or evening to all ForexLive traders and welcome to the start of the new FX week.

As is usual for a Monday morning, market liquidity is very thin until it improves as more Asian centres come online … prices are liable to swing around, so take care out there.

Note that is a New Zealand holiday today, so FX is thinner than its unusually skinny self at this time.

Indicative rates, not a lot changed from late Friday levels:

- EUR/USD 1.0800

- USD/JPY 153.05 – Spiked higher: USD/JPY is above 153 on the Japanese election result – yen plunge

- GBP/USD 1.2974

- USD/CHF 0.8679

- USD/CAD 1.3875

- AUD/USD 0.6617

- NZD/USD 0.5981

This article was written by Eamonn Sheridan at www.forexlive.com.

USD/JPY is above 153 on the Japanese election result – yen plunge

407562 October 28, 2024 03:14 Forexlive Latest News Market News

USD/JPY is just above 153.00, a 70 or so point jump from its late Friday level.

The Japanese election in summary:

- Japan’s ruling Liberal Democratic Party (LDP) and its coalition partner Komeito have, combined, lost their majority

- LDP had a majority in its own right going into the election, gone now of course

- LDP and Komeito have 208 seats

- 22 seats left to declare

- A party needs a majority of 233 seats in the lower house of Parliament, the Diet, to govern alone. Even LDP + Lomeito have not reached this threshold

- the largest opposition party, the Constitutional Democratic Party (CDP), won 143 seats

Counting will continue soon.

The result of the general election has triggered uncertainty about how the world’s fourth-largest economy will be governed. As I posted on Thursday in my preview (ruling LDP could lose up to 50 of its 247 seats) it looks like LDP + Komeito will negotiate with a small party to get across the 233 line.

This article was written by Eamonn Sheridan at www.forexlive.com.

Israel strikes on Iran don’t look designed to minimize the chance of retaliation

407561 October 27, 2024 21:30 Forexlive Latest News Market News

Weeks of speculating about how Israel would respond to Iran’s attacks had markets worried about strikes on energy infrastructure or something that would spark a broader war.

Instead, the attacks look to be measured and US President Biden immediately called for a halt to escalation.

Reports from Iran say the attacks caused only limited damage and Supreme Leader Ayatollah Ali Khamenei didn’t sound eager for a further fight, though the comments certainly didn’t rule it out.

“The evil committed by the Zionist regime (Israel) two nights ago should

neither be downplayed nor exaggerated”, IRNA cited Khamenei as saying.

The Iranian Foreign Ministry said Iran would respond to the airstrikes,

calling them a clear violation of international law and asserted the right to self-defense.

Missile factories were supposed targets along with other military sites, including air defense.

It’s hard to judge what will come next but I expect the oil market to take this at as a negative at the open. Crude was curiously bid on Friday despite the risk-off tone so I’d imagine about $2 of downside, though I also suspect the market had already sniffed out that energy infrastructure wouldn’t be hit.

This article was written by Adam Button at www.forexlive.com.

Weekly Market Outlook (28-01 November)

407560 October 27, 2024 15:30 Forexlive Latest News Market News

UPCOMING

EVENTS:

- Tuesday: Japan Unemployment Rate, US Job Openings, US

Consumer Confidence. - Wednesday: UK Budget, Australia Q3 CPI, Germany CPI, Eurozone

Q3 GDP, US ADP, US Q3 GDP. - Thursday: Japan Industrial Production and Retail Sales,

Australia Retail Sales, China PMIs, BoJ Policy Decision, Switzerland

Retail Sales, French CPI, Eurozone Flash CPI, Eurozone Unemployment Rate,

Canada GDP, US PCE, US Jobless Claims, US ECI. - Friday: Australia PPI, China Caixin Manufacturing PMI,

Switzerland CPI, Switzerland Manufacturing PMI, US NFP, Canada

Manufacturing PMI, US ISM Manufacturing PMI,

Tuesday

The US Job

Openings is expected at 7.990M vs. 8.040M prior. The last report surprised to the upside with the quits rate ticking

slightly lower and the hiring and layoffs rates remaining stable. It’s a labour

market where at the moment it’s hard to find a job but there’s also low risk of

losing one.

The US Consumer

Confidence is expected at 99.3 vs. 98.7 prior. The last report surprised with a big miss. Dana M. Peterson, Chief

Economist at The Conference Board said: “Consumer confidence dropped in

September to near the bottom of the narrow range that has prevailed over the

past two years. September’s decline was the largest since August 2021 and all

five components of the index deteriorated.”

“Consumers’

assessments of current business conditions turned negative while views of the

current labour market situation softened further. Consumers were also more

pessimistic about future labour market conditions and less positive about

future business conditions and future income.”

“The deterioration

across the Index’s main components likely reflected consumers concerns about

the labour market and reactions to fewer hours, slower payroll increases, fewer

job openings—even if the labour market remains quite healthy, with low unemployment,

few layoffs and elevated wages.”

“The proportion of

consumers anticipating a recession over the next 12 months remained low but

there was a slight uptick in the percentage of consumers believing the economy

was already in recession.” Watch also the Present Situation Index as it generally leads the Unemployment Rate.

Wednesday

The Australian Q3

CPI Y/Y is expected at 2.9% vs. 3.8% prior, while the Q/Q measure is seen at

0.3% vs. 1.0% prior. The RBA though is focused on the underlying inflation

measures, so the Trimmed Mean figure will be the one to watch. The Trimmed Mean

CPI Y/Y is expected at 3.5% vs. 3.9% prior, while the Q/Q measure is seen at

0.7% vs. 0.8% prior.

As a reminder, the

RBA delivered a slightly less hawkish hold at the last policy decision, which

is a tiny move towards a more dovish stance, although they don’t see inflation

returning to target for another year or two.

The US ADP is

expected to show 115K jobs added in October vs. 143K in September. The last report surprised to the upside triggering a hawkish

repricing in interest rates expectations. Although the ADP has a poor track

record in predicting the NFP data, the recent market’s sensitivity to labour

market data makes it a bit more important.

Thursday

The BoJ is

expected to keep interest rates unchanged. The central bank toned down its

hawkish stance since the last policy decision and the economic data has yet to

show inflationary threats. Therefore, it’s unlikely that we will see a rate

hike anytime soon and the JPY faith will be shaped by what happens in the US in

the next two weeks.

The Eurozone Flash

CPI Y/Y is expected at 1.9% vs. 1.7% prior, while the Core CPI Y/Y is seen at

2.6% vs. 2.7% prior. The market’s pricing is already very dovish for the ECB,

so we will likely need a very soft report to see the market price in some more

easing.

A hot report

though will likely take off the table the 16% probability of a 50 bps cut in

December. We will also see the Eurozone Unemployment Rate which is expected to

remain unchanged at 6.4%.

The US PCE Y/Y is

expected at 2.1% vs. 2.2% prior, while the M/M measure is seen at 0.2% vs. 0.1%

prior. The Core PCE Y/Y is expected at 2.6% vs. 2.7% prior, while the M/M

figure is seen at 0.3% vs. 0.1% prior.

Forecasters can

reliably estimate the PCE once the CPI and PPI are out, so the market already

knows what to expect. Besides, this report won’t change anything for the

Fed as they are going to cut by 25 bps at the November meeting no matter what.

The market’s

focus is now on the US election.

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

after an improvement in the last two months, spiked to the cycle highs in the

last couple of weeks due to distortions coming from hurricanes and strikes.

This week Initial

Claims are expected at 233K vs. 227K prior, while Continuing Claims are seen at

1880K vs. 1897K prior.

The US Q3

Employment Cost Index (ECI) is expected at 0.9% vs. 0.9% prior. This is the

most comprehensive measure of labour costs, but unfortunately, it’s not as

timely as the Average Hourly Earnings data. The Fed though watches this

indicator closely.

Although wage

growth remains high by historical standards, it’s been easing for the past two

years, and it’s expected to continue to do so given the fall in the job quit

rate.

Friday

The Swiss CPI Y/Y

is expected at 0.8% vs. 0.8% prior, while the M/M measure is seen at 0.0% vs.

-0.3% prior. Although inflation in Switzerland has been within the SNB’s 0-2%

target for more than a year, it keeps on falling steadily with the Core measure

standing around 1% now.

The market is

pricing at 27% chance of a 50 bps cut in December and a soft report will likely

raise those probabilities to roughly 50%. The central bank mentioned that the

CHF strength has been a major drag on inflation but hasn’t taken any real

action to address this problem yet.

The US NFP is

expected to show 123K jobs added in October vs. 254K in September and the

Unemployment Rate to remain unchanged at 4.1%. The Average Hourly Earnings Y/Y

is expected at 4.0% vs. 4.0% prior, while the M/M measure is seen at 0.3% vs.

0.4% prior.

This is going to

be a tricky report given the distortions from hurricanes and strikes in

October. Thankfully, the market is unlikely to care that much given the focus

on the US election.

The US ISM

Manufacturing PMI is expected at 47.6 vs. 47.2 prior. The New Orders index

should be the one to watch as it should be the first to respond to the recent

developments. The latest S&P Global Manufacturing PMI improved a little with new orders ticking higher

albeit remaining in contractionary territory.

Businesses

continue to mention uncertainty around the US election, so you can see why the

market is so much focused on it. Although the data will still have an

impact this week, everything hinges on the US election.

This article was written by Giuseppe Dellamotta at www.forexlive.com.

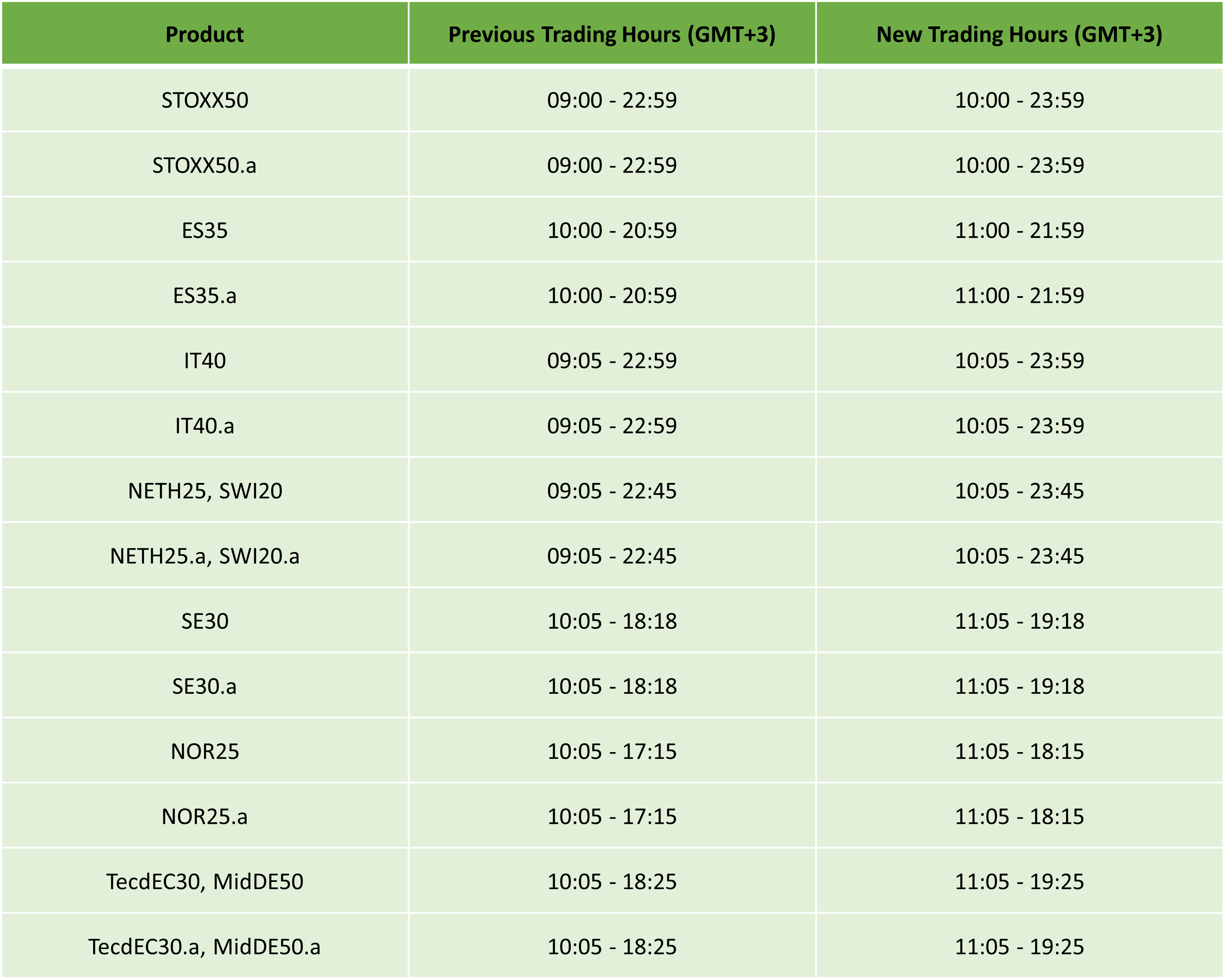

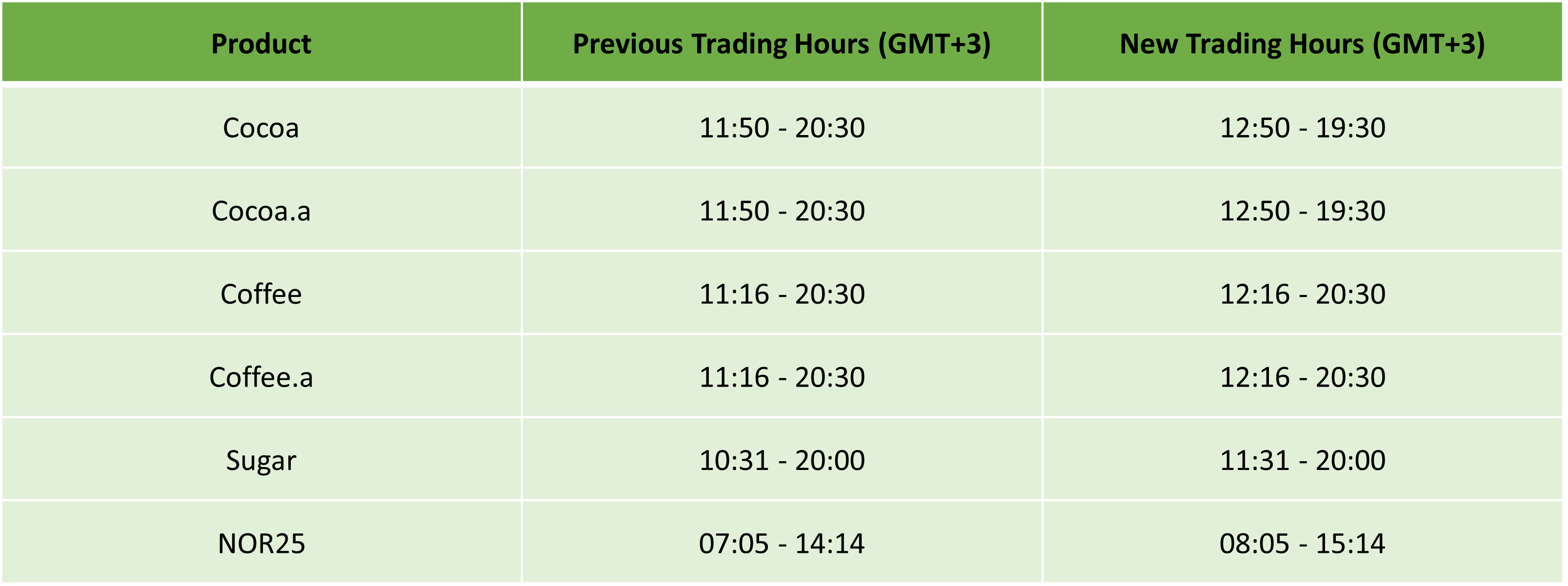

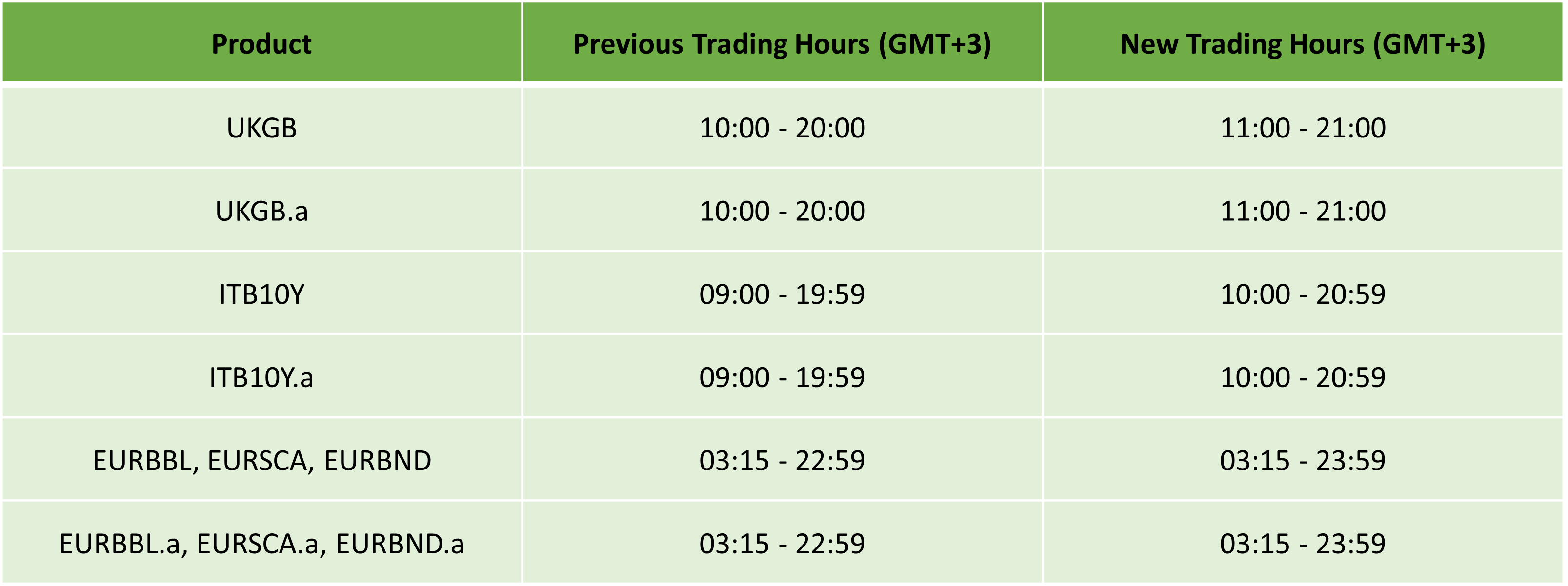

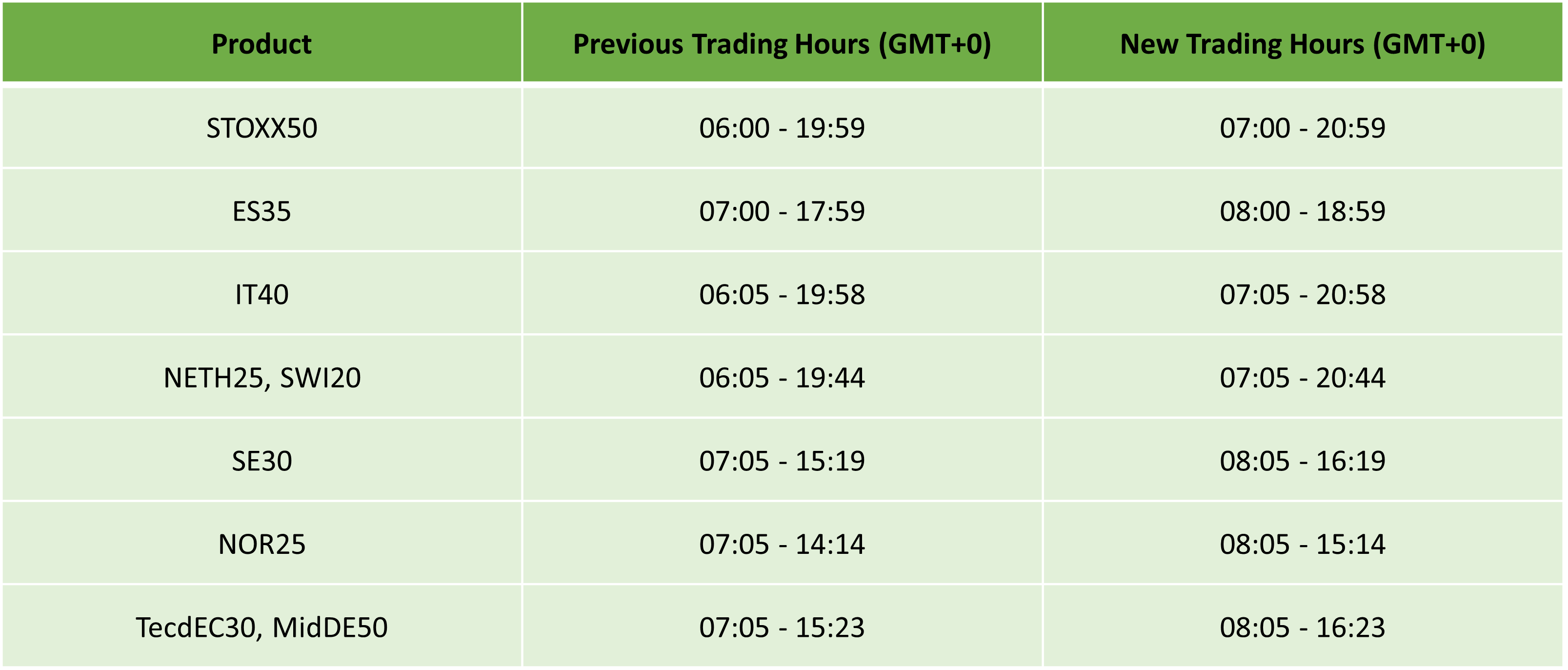

Europe Daylight Saving: Trading Schedule 2024

407554 October 26, 2024 14:00 ICMarkets Market News

Dear Client,

As part of our commitment to providing the best trading experience to our clients, we want to inform you there will be an adjustment in the trading schedule due to the Europe entering Daylight Saving on Sunday, 27 October 2024.

While trading, most products will remain unaffected; however, there will be a change in the trading hours of some products.

MT4/5:

Indices:

Soft Commodities Futures:

Bonds:

Shares:

cTrader:

For any further assistance, please contact our Support Team.

Kind regards,

IC Markets Global.

The post Europe Daylight Saving: Trading Schedule 2024 first appeared on IC Markets | Official Blog.

Forexlive Americas FX news wrap: Consumer sentiment edges higher but market sentiment sags

407553 October 26, 2024 03:45 Forexlive Latest News Market News

- US UMich October final consumer sentiment 70.5 vs 69.0 expected

- US September durable goods orders -0.8% versus -1.0% expected

- Canada August retail sales +0.4% vs +0.5% expected

- Canada Sept new housing price index 0.0% vs 0.0% prior

- Baker Hughes US oil rig count -2

- BOC Macklem: If population grows slows more than assumed, headline GDP will be lower

- CNN: Trump 47%. Harris 47%. It’s a horse race.

- Nvidia is once again the world’s most-valuable company

- Atlanta Fed Q3 GDPNow 3.3% vs 3.4% prior

- ECB’s Lagarde: Disinflation process is well on track

Markets:

- Gold up $8 to $2743

- US 10-year yields up 3.6 bps to 4.23%

- WTI crude oil up $1.43 to $71.63

- S&P 500 flat

- USD leads, NZD lags

The mood steadily soured throughout US trade and NZD and AUD finished at the lows. The S&P 500 rose as much as 50 points but gave it all back to finish flat.

There wasn’t a catalyst for the change in mood that saw steady US dollar buying and bond selling. Perhaps it’s angst about the election of something happening in the Middle East on the weekend. It’s the time in the election cycle when there is often a big surprise and nerves are frayed.

The shape of the move was steady and most pairs grinded lower against the dollar, including the uro which slid to 1.0795 from 1.0835.

A winner on the day was gold, which finished at the best levels and climbed $25 from the lows despite the dollar strength. It’s had an impressive run, hit a record high earlier int the week and today’s close will be the best weekly close ever.

Crude also bucked the trend in risk assets, perhaps in a sign of Middle East worries or position squaring. It rose more than $1 in US trading including a curious spike late just before midday.

USD/CAD finished at its highest since early August and the highest weekly close since 2020 in the fourth weekly decline. A series of highs over the past two years stretch up to 1.3975 but those are now within striking distance in what could be a major break.

In contrast, AUD/USD finished at the lowest since August but has 400 pips of breathing room before the post-pandemic lows. That pair could be in focus in the weeks ahead if China delivers on the fiscal side of stimulus or disappoints.

This article was written by Adam Button at www.forexlive.com.

US equity close: Strong finish falls flat

407552 October 26, 2024 03:14 Forexlive Latest News Market News

A strong gap higher at the open quickly turned into a day of disappointment for bulls. After surging nearly 50 points in early trading to hit 5860, sellers stepped in and methodically unwound those gains throughout the session. The late morning and early afternoon saw particularly steady selling pressure, though buyers did attempt to defend the 5820 level multiple times. A late-day drift lower saw the index ultimately close down just 2 points, a round trip that essentially erased virtually all of the day’s moves.

The weak close despite the strong open could be a warning sign for bulls heading into next week’s trading.

- S&P 500 flat

- NASDAQ Comp +0.6%

- Russell 2000 -0.5%

- Dow Jones Industrial Average -0.6%

On the week:

- S&P 500 -1.0%

- NASDAQ Comp +0.2%

- Russell 2000 -3.0%

This week’s decline in the S&P 500 breaks a six-week winning streak.

Next week is a huge one for the stock market with 5 of the Mag 7 reporting.

This article was written by Adam Button at www.forexlive.com.

Reminder: Elections are tough to predict

407551 October 26, 2024 03:00 Forexlive Latest News Market News

The New York Times released a poll today showing Trump and Harris deadlocked. That’s bad news for the Harris campaign as she had previously been leading. Combined with betting odds shifting in Trump’s favor and it’s starting to feel like we’ve hit a tipping point.

The bond market has been selling off steadily today, which reads like a Trump trade. At the same time, the stock market has been selling off steadily after opening higher and is down on the week.

So what gives? Surely there are some people making election bets but real money knows better. Elections are very tough to predict.

I think we all remember the polling errors in 2016 and 2020 but here is a reminder from Bespoke of what the polls looked like in 2012, which ended up being a 4-point win for Obama and 332-206 in the electoral college.

The kicker here is that betting markets had Obama as a decided favorite, even in the final week as the polls tightened. Right now, betting sites are at about 60:40 for Trump.

As I often say: There is always another trade. Politics and betting on binary outcomes is a tough way to make money in markets. All the best trades on the election are going to be after the results are clear, just like in the last two elections.

This article was written by Adam Button at www.forexlive.com.

Super week coming up: Jobs data, tech titans, and two major GDP reports

407550 October 26, 2024 02:30 Forexlive Latest News Market News

The Fed blackout starts at midnight but the week ahead is packed with market-moving data, decisions and earnings reports.

Here’s a day-by-day preview of the week ahead:

MONDAY, OCTOBER 28

- US data: Dallas Fed manufacturing activity

- UK: Lloyds Business Barometer

- Japan: Jobless rate, job-to-applicant ratio

- ECB’s Wunsch speaks

- Earnings: Ford, Waste Management

- US Treasury Quarterly borrowing estimates, 2yr ($69bn) and 5yr ($70bn) note auctions

TUESDAY, OCTOBER 29:

- US: JOLTS job openings, Conference Board consumer confidence (98.7 prior)

- UK: Consumer credit, M4 money supply

- Germany: GfK consumer confidence

- Tech earnings: Alphabet (Google), AMD

- Others: McDonald’s, Pfizer, BP, Visa, PayPal

WEDNESDAY, OCTOBER 30

Big data day:

- US: Q3 GDP first reading, ADP employment

- Eurozone: Q3 GDP

- Germany: CPI, Q3 GDP

- France: Q3 GDP

- Australia: Q3 CPI

- Tech earnings: Microsoft, Meta

- Others: Boeing, Volkswagen, BASF

- UK Autumn Budget

- US Treasury quarterly refunding announcement

THURSDAY, OCTOBER 31

- Bank of Japan policy decision

- US: PCE inflation (core seen +0.28% MoM)

- Eurozone: CPI, unemployment

- China: Official PMIs

- Heavyweight earnings: Apple, Amazon, Intel, Samsung

- Energy: Shell, TotalEnergies, ConocoPhillips

- Others: Mastercard, Merck

FRIDAY, NOVEMBER 1

- US: Nonfarm payrolls (some forecasts as low as 0K, consensus at +123K), ISM manufacturing

- China: Caixin manufacturing PMI

- Switzerland: CPI

- Earnings: Exxon Mobil, Chevron

The week’s big focus will be on the US jobs report Friday, but markets will have plenty to digest before then with Q3 GDP, inflation data, and massive tech earnings. With five of the “Magnificent 7” reporting (representing $12 trillion in market cap), expect some volatility in equity and currency markets throughout the week.

This article was written by Adam Button at www.forexlive.com.

Gold climbs to the highs of the day, poised for weekly record close

407549 October 26, 2024 01:14 Forexlive Latest News Market News

Gold is impressive once again today as it rises $8 to $2743 after earlier falling as low as $2717. The rebound virtually assures that it will break the weekly closing record of $2719 set just a week ago.

It’s been record after record for gold and on Wednesday it touched the best-ever at $2758 before a round of profit taking.

I spoke with Kitco News about gold this week and highlighted a number of trends behind the rally. The election is top of mind at the moment but both candidates promise to antagonize trading partners and rivals. This week’s BRICS summit highlighted the efforts to shift trade outside of borders.

One of the points I made in the interview was that the biggest long-term threat to the US dollar might be the intellectual property system, particularly in a world where AI is doing all the inventing. An enlarged BRICS could mutually invalidate patents, putting them at odds with the US and under threat of retaliation.

That’s certainly not a trade for today but a black swan that I think is probable in the next decade.

This article was written by Adam Button at www.forexlive.com.

1739 | +0.611% | GBPUSD

407454 October 26, 2024 00:48 SwingFish Trading Room Journal GBPUSD

Today’s risk: 0.32% [True drawdown: -0.0292%] (more…)

Full Article